May 2020

An unprecedented intentional shutdown of the U.S. economy has brought the market into uncharted territory. Unlike the three most recent major market meltdowns (Crash of 1987, Tech Bubble and Global Financial Crisis), the current crisis was not initiated from within financial markets. While it is still too early to tell the lasting effects that the pandemic will have on the economy, we have seen markets rebound from their lows and it is possible that we have seen the worst of the largely self-induced recession.

Market crashes are typically accompanied by a rotation in leadership, but because this has not been a conventional economic recession, this recovery may be different. Over the past few years, we have periodically identified areas of the equity market that were potentially problematic or anomalous and a potential source of unintended risk. We don’t yet know which trends from before the market crash are strong enough to carry through and what new trends may emerge, but there are some telling features from the recent market activity that are worth drawing out.

Size Factor

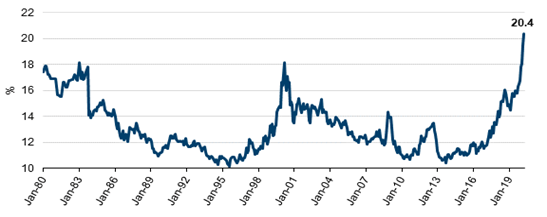

We had written extensively about the issue of size and concentration risk before the onset of the pandemic. The current crisis pushed investors even more towards large, financially stable companies, especially those with a large presence in the digital world. In other words, the same type of companies that were driving the market prior to the crash. As of April 30, the concentration of the five largest companies in the S&P 500 stood at 20.4%, an all-time high.

___________________________________________________________________________________

Exhibit 1: Concentration of the largest 5 companies in the S&P 500

Source: S&P Global; Columbia Threadneedle Investments. As of April 30, 2020.

While the continued performance of Facebook, Apple, Amazon, Netflix, Google, and Microsoft stocks is noteworthy, it masked the fact that after a long run of underperformance, the S&P 500 Equal-Weight Index outperformed the capitalization-weighted S&P 500 by 1.6% during April, as smaller-cap stocks recovered.

Idiosyncratic risk

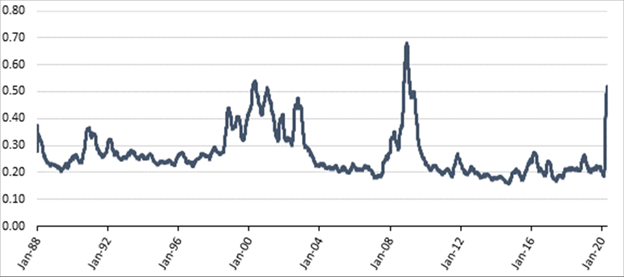

Active stock selection can make the greatest contribution when idiosyncratic risk (unrelated to beta) becomes a bigger component of total volatility. In times of market panic, some investors may choose to sell first and ask questions later, creating market inefficiencies and thus buying opportunities.

____________________________________________________________________________________

Exhibit 2: Cross-sectional idiosyncratic risk within S&P 500

Source: Columbia Threadneedle Investments; as of April 30, 2020. Idiosyncratic risk is the average of the annualized standard deviation of their Beta-adjusted daily returns in the past 3 months, for all S&P 500 stocks.

Many active managers have a wish list of companies that are beyond their current price/valuation targets. Sharp market corrections like the one we just experienced made this a buying opportunity for some managers. In Exhibit 2, you can see that the market’s idiosyncratic risk reached a level not seen since the financial crisis.

Factor diversification

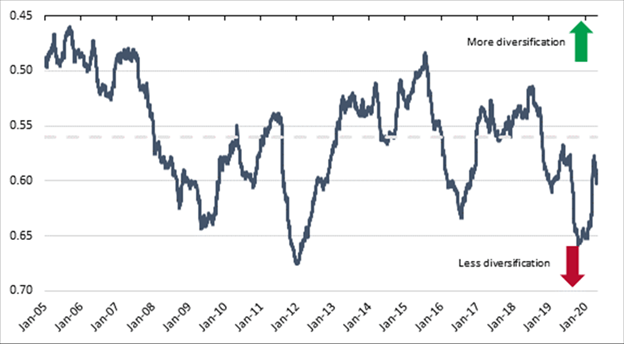

Despite still seeing high levels of size concentration in the indexes, we have begun to see a greater amount of factor diversification among stocks. Factor diversification is one way to look at market movements that are not explained by beta and is one indication that there is more discrimination among buyers, i.e., less reliance on buying baskets of stocks.

____________________________________________________________________________________

Exhibit 3: Factor diversification index – factor investing moving closer to normal levels

Data as of April 30, 2020.

Source: Columbia Threadneedle Investments; Axioma; S&P 500 universe; Factor diversification is defined as the percentage of variance explained by the first three principal components of the returns of 11 Axioma measures of risk over a rolling 6-month period. The higher the explained variance, the lower the factor diversification, and vice versa. The dotted line equals the average of the period from January 1, 2005.

Remember that prior to the pandemic’s outbreak, markets had reached new highs—the S&P 500 was up 5% for the year as of the February 19 close—and valuations were extended. Combined with the justified response to the massive slowdown in the global economy was also a revaluation of stock markets, which we are still working through. Some companies fell to prices that were unthinkable six months ago and we have already seen a rebound among stronger companies.

Factor valuation

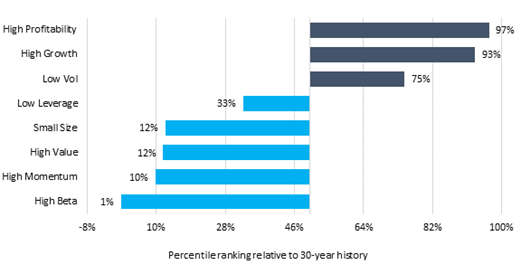

The market of the last ten years has been characterized by performance bifurcation, notably among growth/value and large/small, but in other areas as well. While these factors did not experience a notable change over the last few months, Momentum, which was a notable market driver over the last few years, did. As earnings estimates were revised lower at a rate not seen since the financial crisis, Momentum ended the month at the lowest 10% of its valuation over the last 30 years. Exhibit 4 shows where certain factors currently sit in their historical timeframe.

____________________________________________________________________________________

Exhibit 4: Factor valuation – Current valuation of different factor strategies

Source: Axioma and Columbia Threadneedle Investments; S&P 500 universe. Factor valuation spread is defined as the ratio between the median forward 12-month P/E ratio for the top 20% of stocks with the highest factor scores, and that for the bottom 20% — no sector standardization. The spreads are ranked against their monthly history during the period between January 1990 and April 2020. A high percentile ranking means more expensive in historical terms. Data as of April 30, 2020.

Conclusion

While we are still early in the recovery to draw too many conclusions, we have seen a major revaluation of some companies, but we have not seen the type of rotation we saw in the last two bubbles (technology/telecommunications and real estate/financials) perhaps because of the atypical nature of this recession. Our Value models performed well in April, but the rotation was not particularly strong and still significantly lags Quality year to date. What we will continue to monitor is whether this current recession continues to bifurcate the market or if we will see a true rotation/diversification of factors.

By Mark Kelly, in conjunction with Jason Wang, Columbia Threadneedle Head of Quantitative Research